The regularization of water conditions in part of the agricultural area, together with an improvement in grain prices because of the temporary reduction of withholding taxes, has not yet been transferred to the Argentinean fertilizer market.

‘During this week the demand for fertilizers in the Argentinean market remained practically paralyzed as a result of the intense drought that affects a large part of the productive areas of the country,’ says the latest report from a local specialized consulting firm.

The demand from producers is very limited both in terms of fertilization of late corn and early purchases for the 2025/26 fine season.

While some agricultural areas were blessed by recent rainfall, others are still waiting for water inputs with fair to poor soil moisture reserves.

While on the international market the values of granulated urea continue to show an upward trend, in the Mercosur regional market prices remain flat due to weak demand for the nutrient.

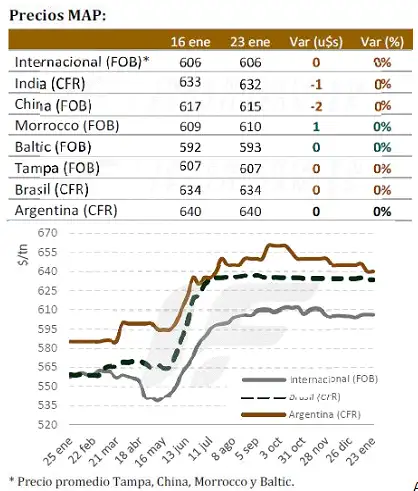

As for the prices of phosphate fertilizers (MAP and DAP), they remained stable during the week. ‘Although no new business has been registered in Argentina, there are beginning to be enquiries for pasture fertilization, which could indicate a gradual change in demand,’ the report says.

It is worth noting that, thanks to the orderly exchange market implemented by the present government, the wholesale values of fertilizers no longer have major overpricing caused by the problems arising from the difficulties of access to foreign exchange by importers during the previous administration’s Minister of Economy.

Official Argentine fertilizer import data for the year 2024 are now available and show that imports of granulated urea reached 1.05 million tonnes last year, a year-on-year increase of 36%. This is a volume that is close to 2020 levels, although still far from the record high recorded in 2021, when imports totalled 1.53 million tonnes.

UAN and ammonium thiosulphate (ATS) imports in 2024 stood at 330,000 tonnes, similar to those recorded in 2023, but significantly below the 2020 record volumes of 700,000 tonnes.

In 2024, imports of MAP and DAP totalled 1.06 million tonnes, an increase of 8% over 2023. However, these volumes are significantly lower than the 1.33 million tonnes in 2021.

The EU’s growing dependence on Russian nitrogen fertilizers and the implications of new tariffs

The European Union has historically relied on Russian gas as a key input for its domestic nitrogen fertilizer production. However, over the past three years, its dependence has extended beyond raw materials to include the direct import of Russian nitrogen-based fertilizers.

EU import data underscores this increasing reliance:

⦁ 2021: The EU imported approximately 2.33 million metric tonnes of nitrogen fertilizers from Russia.

⦁ 2022: Imports increased to 2.56 million metric tonnes.

⦁ 2023: A slight dip saw imports decline to 2.44 million metric tonnes.

⦁ First half of 2024: The EU imported 2.56 million metric tonnes in just six months, matching the total volume for the entire year of 2022.

This trend suggests a significant shift in the EU fertilizer supply chain, raising concerns about strategic vulnerabilities and market concentration.

The European Commission’s response: New tariffs on Russian and Belarusian fertilizers

In light of these import trends, the European Commission has proposed new tariffs on nitrogen fertilizers and agricultural products from Russia and Belarus. If approved, these measures would add an additional 30% duty on top of the existing 6.5% import tariff, effectively making Russian fertilizers significantly more expensive for European buyers.

If these tariffs are imposed before the spring application season, the implications for supply, pricing, and global trade patterns could be profound. The key question remains: who stands to benefit from these restrictions?

Potential winners in a changing market

Reflecting on 2022, when the EU temporarily lifted its 6.5% import duty for all producers except Russia and Belarus, several new suppliers stepped in to meet demand. A similar scenario could unfold if the new tariffs take effect. The likely beneficiaries include:

⦁ Nigeria: Geographically well-positioned to supply Europe and expanding its nitrogen production capacity, Nigeria could emerge as a significant alternative supplier.

⦁ Egypt and Algeria: Both countries already have a strong presence in the European market and may strengthen their positions further.

⦁ Arabian Gulf producers: Fertilizer producers from countries like Saudi Arabia, Qatar, and the UAE will likely seek to capture a larger share of the EU market.

Russia’s next moves: Diversifying export markets

Despite potential losses in the European market, Russia has been expanding its footprint elsewhere:

⦁ Latin America: Russian fertilizers have gained traction in Mexico, Argentina, and Brazil.

⦁ India: Russian producers have actively participated in government tenders, securing a foothold in one of the world’s largest fertilizer markets.

⦁ Turkey and the US: Both markets have seen increased Russian supply in recent years.

⦁ East Africa and Southeast Asia: These regions are expected to become the next strategic focus for Russian fertilizer exports as Moscow seeks to offset potential losses from the EU market.

Conclusion: a potential reshaping of global fertilizer trade

If the proposed EU tariffs are implemented, the European nitrogen fertilizer market could undergo a fundamental transformation. While alternative suppliers are poised to step in, Russian exporters will likely intensify their efforts to penetrate new markets, further shifting global fertilizer trade dynamics.

Ultimately, the effectiveness of these tariffs will depend on Europe’s ability to secure alternative supplies without significantly increasing fertilizer costs for farmers. As spring application season approaches, all eyes will be on Brussels’ next move and its impact on European agriculture and the global fertilizer trade.

ARGENTINA MAIN CROPS OVERVIEW:

SOYBEANS: As of this report, 67% of the soybean-planted area is in Normal/Excellent crop condition, reflecting a weekly decline of nearly 4 percentage points. However, widespread rainfall in recent days, with significant accumulations in the central region, has led to a 6 p.p. increase in Adequate/Optimal water condition, now covering 64% of the planted area. These timely rains benefit 39% of the area currently in critical yield-defining stages, mainly in the central agricultural region. This moisture supply is expected to halt potential yield losses for first-crop soybeans and alleviate water stress before critical stages in second-crop soybeans.

CORN: For corn, the current planting cycle is nearing completion, with 99.3% of the projected 6.6 million hectares already sown. Over the past week, planting progress was 0.6 p.p., with only a few remaining lots to be incorporated in the NEA region. Despite recent rains targeting the most drought-affected areas, early planted corn remains unable to recover, given its advanced phenological stage, though some benefit may be observed during grain filling. However, for late-planted fields in southern Córdoba and western Buenos Aires, where 50-60% of the area is entering its critical period, there has been a 21 p.p. increase in Optimum/Favourable moisture condition, which is expected to improve crop condition in the coming days. Meanwhile, initial harvests in the Central-East of Entre Ríos have reported good results. Under this scenario, the production estimate remains at 49 million tons.

SUNFLOWER: Sunflower harvesting now covers 8.4% of the suitable area, after a weekly progress of 1.2 p.p. The average yield has reached 2.14 Ton/Ha, allowing the production estimate to remain at 4.1 million tons. Despite the recent rains, which were mainly concentrated in the central agricultural region, 53.7% of the standing crop still exhibits Poor/Dry conditions. However, given sunflower’s resilience to moisture limitations, 91.6% of the standing crop remains in Normal/Excellent condition. Additionally, 67.4% of the crop is in flowering and grain-filling stages, with isolated reports of caterpillar outbreaks in the southern agricultural region, maintaining high yield expectations.