The situation of the fertiliser market in Argentina reflects a scenario of uncertainty and low activity, while international prices continue to rise.

Fertilisers in Argentina: low demand and rising international prices

According to the latest report from IF Ingeniera en Fertilizantes SA, local demand remains limited, with agricultural producers waiting for rains and better economic signals to make decisions on fertilisation and future purchases.

Local market in recession:

Local fertiliser demand, particularly for products such as MAP and DAP, has been virtually flat following the end of the coarse crop sowing season. Prices for these inputs remain stable between $780 and $790 FCA, but there is no forward buying interest for the 2025 fine season. In addition, difficulties in the input-output relationship are aggravating the situation and limiting producers’ profitability.

International prices have also affected the local market. Last week, an increase of between $15 and $20 per tonne was recorded, with further upward adjustments expected. However, the lack of rain and uncertainty over economic measures such as devaluation or the reduction of withholding taxes have slowed purchasing decisions.

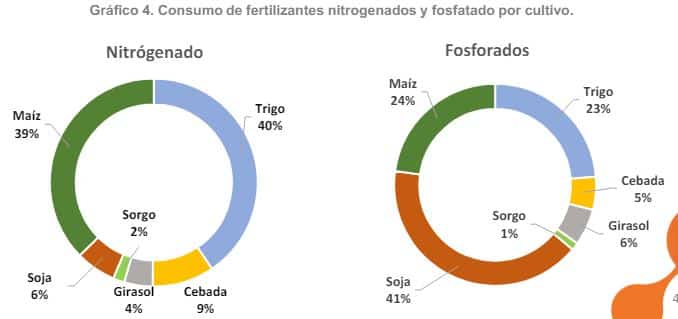

Nitrogen and phosphates: Contrasting markets:

The international nitrogen market is showing strong activity thanks to India’s 1.5 million tonne tender and high European prices driven by gas costs. Urea saw weekly increases of up to 8% on the Argentinean market to reach $515 FCA.

For phosphates, the absence of China as an exporter has kept prices high. India, with low stocks, and other emerging markets, such as South East Asia, have maintained demand for DAP. However, demand for MAP in western markets such as the United States and Brazil remains low.

Input-output ratio: An unfavourable scenario

The relationship between input costs and grain prices remains unfavourable. For example, the urea/wheat ratio is 2.7, while the MAP/corn ratio is 4.1, which further hampers the profitability of agricultural producers.

On a year-on-year basis, urea (-37%) and wheat (-12%) prices have fallen significantly, while the MAP/corn ratio has risen by 43%, a dynamic that complicates fertiliser investment decisions.

The outlook:

The report highlights that although there has been movement in the liquid fertiliser market, demand remains subdued. With a combination of high temperatures and still competitive prices, liquids are presented as a viable alternative for nitrogen fertilisation.

Local producers remain alert to possible adjustments in international prices, agricultural commodities and government policy, while the global market continues to show active momentum led by Indian demand and high European costs.

Source: InfoCampo

Engro Fertilizers further expands

Engro Fertilizers, one of Pakistan’s leading urea producers, inaugurated a new Markaz Centre in Muridke, Punjab, on January 26. This initiative is part of the company’s support for the government’s efforts to ensure the availability of high-quality fertilizers at government-regulated prices. The new center in Muridke joins existing ones in Bahawalpur, Sargodha, and Sahiwal, significantly expanding the reach of services provided to farmers across these regions.

During the inauguration event, the Federal Minister for Industries and Production of Pakistan, Rana Tanveer Hussain, reiterated the government’s commitment to bolstering the country’s agricultural sector and improving farmers’ livelihoods. He emphasized the collaboration between the government and the fertilizer industry to ensure the continuous availability of fertilizers at controlled prices. Hussain praised Engro Fertilizers for their role in establishing Markaz Centres, which aim to curtail hoarding and price manipulation by intermediaries.

Ali Rathore, CEO of Engro Fertilizers, commended the government’s dedication to agriculture and farmer welfare. “Engro Fertilizers is dedicated to enhancing the agricultural sector by ensuring that our farmers have timely access to high-quality fertilizers at official prices,” Rathore stated. He further highlighted the recent launch of the UgAi app, Pakistan’s first integrated agri-e-commerce platform. This platform allows farmers to purchase fertilizers at official prices and utilize advanced drone technology and satellite imagery to monitor crops effectively, reduce costs, and increase yields.

Additionally, in response to the current market dynamics and farmer economics, Engro Fertilizers has announced a temporary off-season sales incentive for urea, supporting the industry’s value chain and ensuring that farmers receive necessary support during critical planting and growing seasons.

Source: Fertilizers Daily

ARGENTINE MAIN CROPS OVERVIEW:

SOYBEANS: In its final stages, soybean planting covers 99.2% of the 18.4 million hectares, with progress still needed in the northern part of the agricultural area. Although recent rainfall has been recorded, mainly in Córdoba, southern Santa Fe, and Entre Ríos, in northern Buenos Aires, it has been heterogeneous in both intensity and distribution. The Normal/Good crop condition has decreased by 7 percentage points, as has the Adequate/Optimal moisture condition, which fell by 5 percentage points, despite the recent rains. The continued lack of moisture and high temperatures, particularly in the

Southern Core and Center-East of Entre Ríos has affected the potential yield of early-planted soybeans. These conditions have also impacted second-crop soybeans in the Southern Core and Northern La Pampa-Western Buenos Aires, resulting in a reduction in plant stand. In this context, a production adjustment was made, reducing it by 1 million

tons, reaching 49.6 million tons.

CORN: Regarding corn intended for grain, planting has covered 98.3% of the national total, following a weekly progress of 3.2 percentage points. The lack of rainfall and the high temperatures recorded during the last weeks of December and throughout January have initially impacted soil moisture and, consequently, the condition of the corn crop, limiting its yield potential. The most affected areas have been in the agricultural center-east, with a critical focus on the districts within the Southern Belt zone and western Buenos Aires. While early planted corn from September managed to avoid the driest period, crops planted in October and early November have been the most affected, as they went through their critical growth phase during the drought. On the other hand, crops planted in December and January are currently in their vegetative stage with lower water demand, showing signs of water stress such as leaf curling, although they could recover if rainfall returns to the region. In this context, the production forecast is reduced to 49 million tons, which is 1 million tons below the previous forecast.

SUNFLOWER: Finally, regarding sunflower, the harvest progress stands at 4.7% of the suitable area, with an average yield of 1,9 tons per hectare. On the other hand, the scarce rainfall and the high-water demand of the crop have significantly reduced

soil moisture reserves. Currently, 45% of the area has Adequate/Optimal moisture conditions, which represents a 10-percentage point decrease compared to the previous week. At the national level, 87% of the area shows Normal/Excellent crop conditions, an 8-percentage point drop compared to the last report. This decline is mainly concentrated in the Southwest of Buenos Aires-South of La Pampa and Southeast Buenos Aires, where the crop’s Regular/Poor condition has increased by 14 and 10 percentage points, respectively.

Source: Buenos Aires Stock Grain